The QR code revolution in payments — what's missing?

Delving into digital payment usage patterns of small vendors, and the role of UX research and design in building financially inclusive products for new smartphone users.

I’m sure most of us can relate to those days in the cash-dependent era when the hunt for the right denominations of notes and coins was real. There have been several instances where I couldn’t fulfill a purchase because the vendor at a neighbourhood store said he doesn’t have change for ₹500 and I had absolutely no other option but to walk back empty-handed. Not to forget the daily dose of rejections from cab and autorickshaw drivers when you reveal that it’s not a cash payment.

Fast forward a few months after the first wave of the pandemic when small businesses had slowly started to reopen and there was suddenly a new element adorning stores—the QR code. I recall stepping out to purchase tender coconut from a pushcart vendor and I had religiously carried the exact amount to avoid problems with change. However, on seeing a QR code placed on the cart, I remember asking if I can pay through Google Pay and he responded almost as if it was obvious. With the lockdown phasing out, there seemed to have been a new revolution. To the extent that I can now walk out of my house with only my phone, without having to worry that I won’t be able to buy things. I was intrigued by this shift from a digital payment averse population to the QR Code becoming widespread on most storefronts. My curiosity led me to understand how small businesses got started using digital payments and how this sudden transition of adopting it happened over a relatively short duration.

To uncover this, I spent some time speaking to pushcart vendors and small business owners in Gandhi Bazaar, a prominent market area in Basavanagudi, Bangalore. Most of these vendors are first-generation smartphone users who have been accustomed to using cash-based transactions for over 30 years now. But they too seemed to have made the switch.

My questions were centered around understanding adoption, frequency of usage, merits, challenges, perceptions about the user interface, and their overall interaction with digital payments. To my surprise, once I began talking to users, I learned that a lot of them have never used payment apps to send money nor have they explored the interface. Their usage was limited to receiving money from customers through the ‘Scan to pay’ option or via phone number at most.

Assumption busted!

I presumed that vendors who accept QR code-based payments are active users of digital payment applications. I also thought that by now several vendors might have explored using digital payments in their personal capacity and would be able to give me a peek into their experience using it.

Here’s what I discovered instead :

Let's begin by broadly categorizing the findings that led to this conclusion under the following heads — Initiation & adoption, Usage, Experience, Trust, and Workarounds.

Initiation and Adoption

So, what led these folks who were almost repulsed by non-cash payments to go ahead and embrace it?

Yes, of course, the Covid-19 pandemic is quite evidently the reason why most vendors began to use digital payments. They noticed that several customers were hesitant to make contact with cash due to safety concerns and began to enquire about making payments through UPI1 based modes.

Now that we know the trigger, you might wonder how exactly the shift happened.

Older vendors rely on their children to help them with the initial set up such as linking their bank accounts. Whereas the ones who feel that comprehending this is beyond them have the money sent to their kid’s account. Some rely on educated family members to get things going initially as they feel that the uneducated cannot get their way around technology.

Moreover, the entire stretch in Gandhi Bazaar has a strong sense of community — what we understand as social capital. These vendors are taking care of family-owned stores that have been present since their grandparents' generation. This tight-knit community model has helped in knowledge sharing amongst peers and some of them were introduced to digital payments by their friends who have set shop in the same vicinity. After seeing others reap the benefits of digital payments, they decided to test the waters and adopted these new modes.

What about non-smartphone users?

A smartphone is undoubtedly a huge investment for many of these retailers, which is why a handful of them have an SMS confirmation system set up on their numbers. Despite not having an app interface to interact with, they highlighted that the SMS confirmation is good enough for them. While most of us might be oblivious to the existence of this, a vendor stated that people from a particular fintech organization had come to install the QR code in his shop and helped him configure this alternate way of receiving notifications for cashless payments.

Usage

We now have a fair sense of how they came about using these new modes, so let's look at the extent to which they use them.

Several shop owners only make use of payment apps to receive money and don’t make use of any other features on these apps. The farthest they have gone is to send money, but beyond that, the rest of the features remain unexplored.

To my surprise, almost none of them were able to answer what else they wish the app could do because they were not aware of the current offerings of these platforms in the first place.

Experience

Let's now dive into what their experience has been like.

Amongst the ones who have steadily accepted digital modes, many expressed that initially, it felt weird because this way of going about transactions was a stark contrast from the tangible mode of payment that they were used to. Some even highlighted that initially, they were suspicious because they were not receiving any tangible money in hand and were ascribing value to a number on the screen. However, after going to the banks and verifying a few times whether they were actually receiving the money, they slowly began to build trust in the system. With time, they also realized it serves the same purpose as cash and felt that it is a safer mode because, unlike physical notes, they cannot lose this and it can’t get stolen either. This made them appreciate its benefits and embrace this new model.

Besides, the acceptance is also because many felt that there’s no way around it. Even if it is challenging to set it up, they have to provide this option to customers otherwise it’ll negatively impact their business.

In terms of interactions with the technology, a fair bunch of them stated that they initially had no idea what each action on the app leads to, but with time they have become familiar with it.

The voice confirmation—Paytm Soundbox, was a crowd favourite and was said to be useful by several vendors because it was as if a human was reassuring them.

Well, it’s not all good though. Let’s discuss what’s not working for them.

Not everyone has accepted this new mode. A few think that digital payments are a bane and they felt their life was better with cash-based transactions. The reasons stated were that sometimes though customers claim to have made the payment, the vendors would not have received the money when they checked their bank accounts. This has led to them undergoing minor losses. Additionally, sometimes due to poor internet connectivity or server downtime, customers cannot make payments and they decide not to go ahead with the purchase.

Another common issue faced is that they cannot use digital modes when they go to wholesale markets to acquire fresh produce. Thus a shift to digital modes has made it more tedious for vendors as they now have to go to the ATM or visit banks to withdraw cash before buying products for the week.

Workarounds

Buying a smartphone can sometimes be worth the entire month's earnings for them. Now what?

To tackle this, some vendors have found alternative ways of going about receiving payments. They ask customers to pay a neighbouring shop owner in case they have not carried cash.

Support and Assistance

What keeps them from abandoning this rather intimidating feat?

Whenever they face any issues with digital payments, they have a contact they can reach out to and that gives them some comfort. Moreover, they also mentioned that from time to time persons from organizations with digital payments in the markets check in with these users personally to ensure everything is working smoothly for them and ask for feedback about their experience.

The role of design research and UX in improving digital experiences for the financially excluded

Now that we have gotten a glimpse into ground realities, let’s look at what we can do to avoid further alienation of these populations from the world of digital payments.

#1 Begin with User Research

It goes without saying that there is no alternative to going on the field and speaking to your users. Some of the discoveries that came to light through the conversations I had with vendors were things I would have never known without asking them the whys and the hows. We generally tend to operate on binary thinking, but that approach overlooks the nuances that can actually add value to product design. For instance, through this field study, I learned that in the context of these vendors, digital literacy and creating awareness about the product are of higher priority than a new app feature that is going to get added to the bucket of unused options on the app. Therefore, to understand their financial behaviour and ensure that your product aligns with their aspirations, conduct user research before you begin product development, while in the midst of it, and even for future iterations.

#2 Help them build digital confidence

As observed, these users experience the internet very differently as opposed to everyday internet users like us. Here’s what we can do to help them break the assumption that technology is only meant for the educated.

Assist them with the initial setup.

Hand-hold them and train them on how to use the application as small wins in the learning process can help them build digital confidence.

This is an essential step because if not done, the simplicity of the app remains unfamiliar territory to new users. Due to this, they might even avoid using these new digital modes as they continue to remain intimidated due to preconceived notions about its complexity. This can lead to higher dropout rates and a fall in daily active usage metrics.

#3 Simplify the onboarding experience

Beyond initial hand-holding, simplify the onboarding experience from the perspective of the app flow to prevent dropout rates before users have explored the app. Lengthy sign-up processes, in conjunction with poor internet connectivity, can lead to immense frustration for new internet users and hence leads to increased app abandonment.

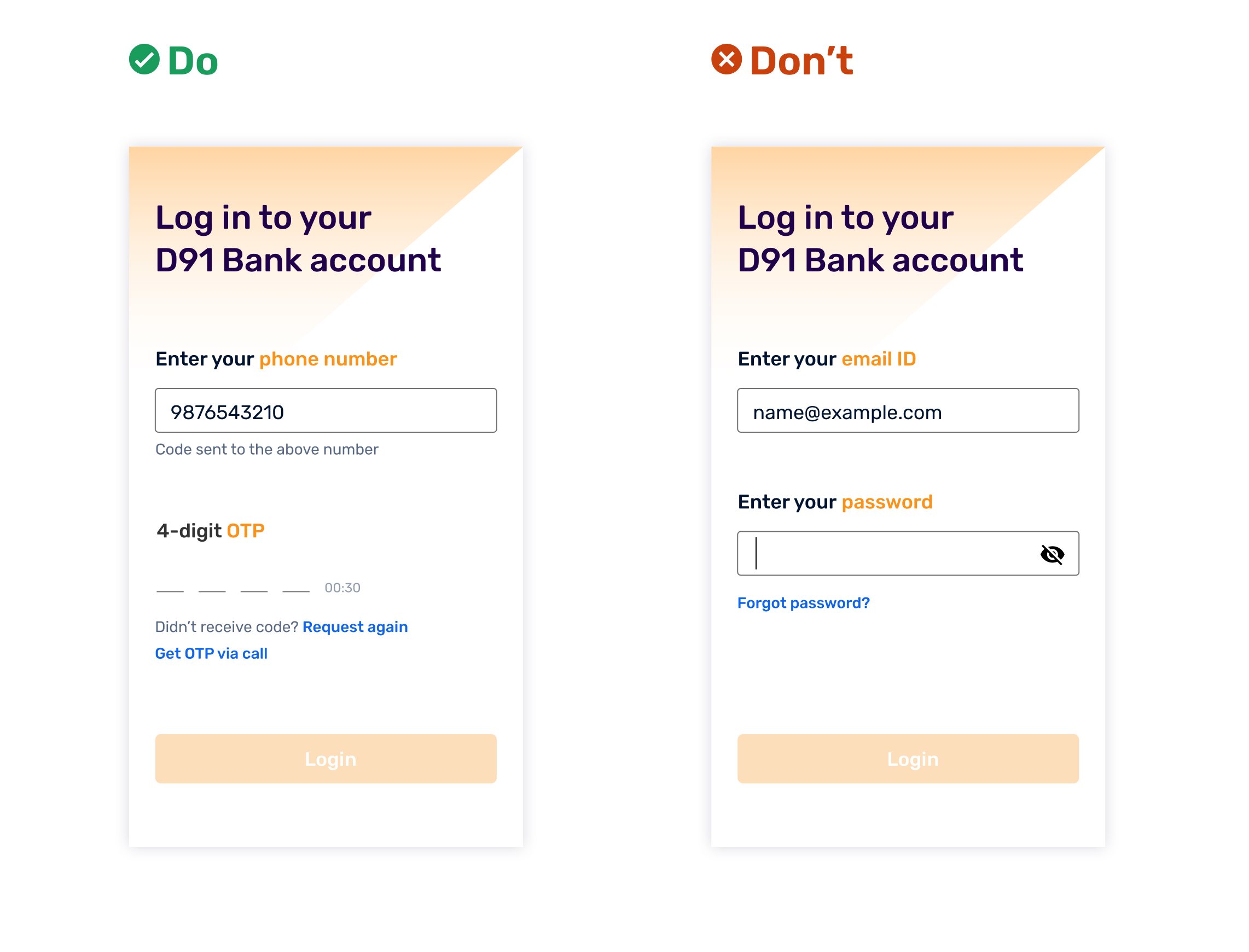

Do not make them think too much. Try to avoid asking them to remember complex pins, instead implement a phone number + One-time password(OTP) login so that they can copy and paste a fresh pin each time and this in turn demands less work from their end.

Display tooltips2 or voice assistance in a vernacular language as they fill out the form. This is extremely useful as it is not possible to provide constant in-person assistance to new internet users.

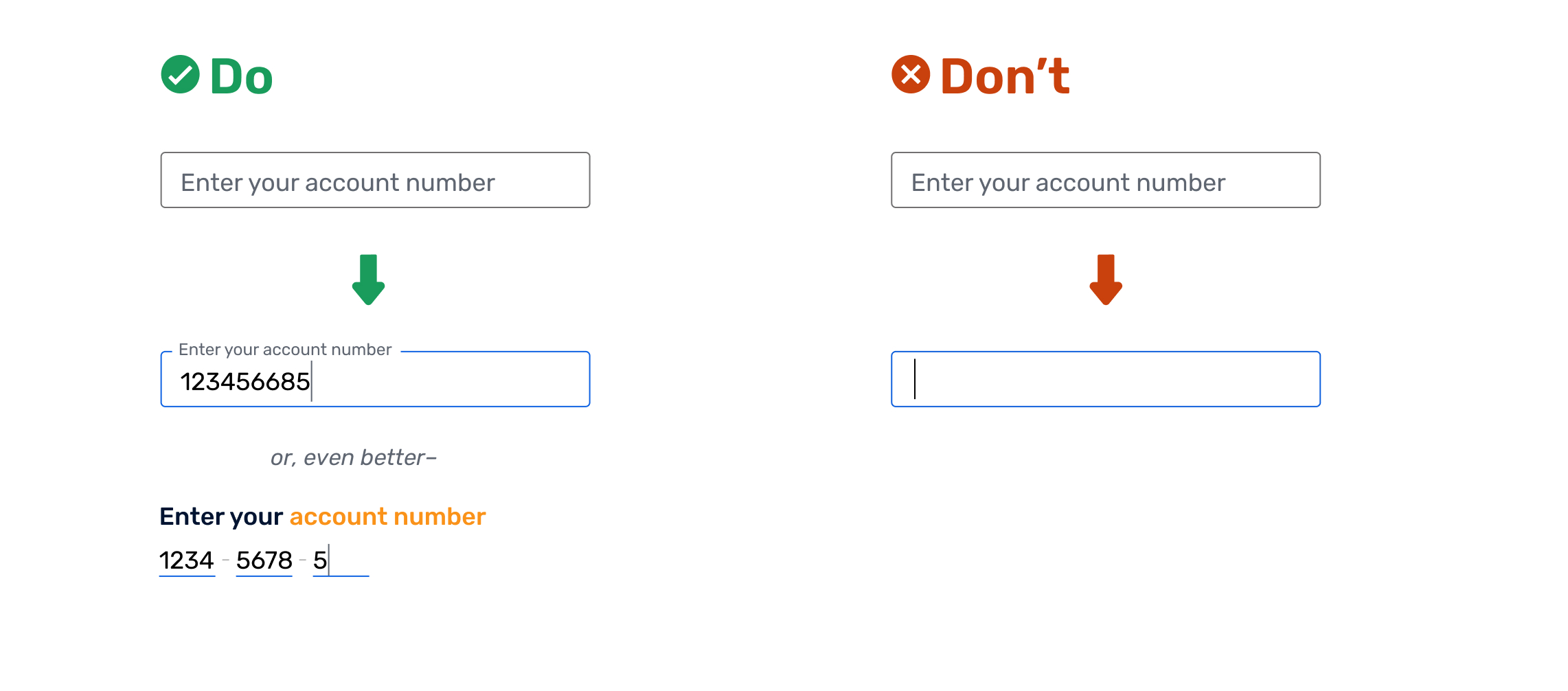

Auto-populate data wherever you can and reduce the number of questions asked. Voice assistants serve as a great alternative due to their human-like assistance qualities.

Tooltips can also be provided on every app launch to help them navigate the app smoothly or include in-app assistance to guide them on where to click.

Including video tutorials that they can refer to whenever they are confused about how to use something is also a great option.

Wherever possible, try to build offline capabilities into your applications so that they can use it despite poor internet connectivity.

#4 Interface and experience design

Try to ensure that in-app processes mimic the processes they follow if they were to do it in person. Interfaces and procedures that better align with their existing practices will increase adoption due to familiarity with the steps involved. On the other hand, complex interfaces will lead to further alienation of the population that already feels excluded from formal finance. Include UI elements that remind them of doing or completing similar procedures manually. For example, consider the bank transfer option on a payment app. If they were to visit a bank to do this, the steps would involve filling a challan, depositing the cash or cheque, and then receiving a stamp that reads ‘paid’. To bring in familiarity, maybe we can make some changes to the nomenclature used within the app by using the term challan and then prompting them to enter recipient details. Additionally, once the transfer is successful, can we use Scalable Vector Graphics (SVG)3 that displays ‘PAID’ rather than a tick mark which a lot of them might not relate to?

#5 Humanising technology

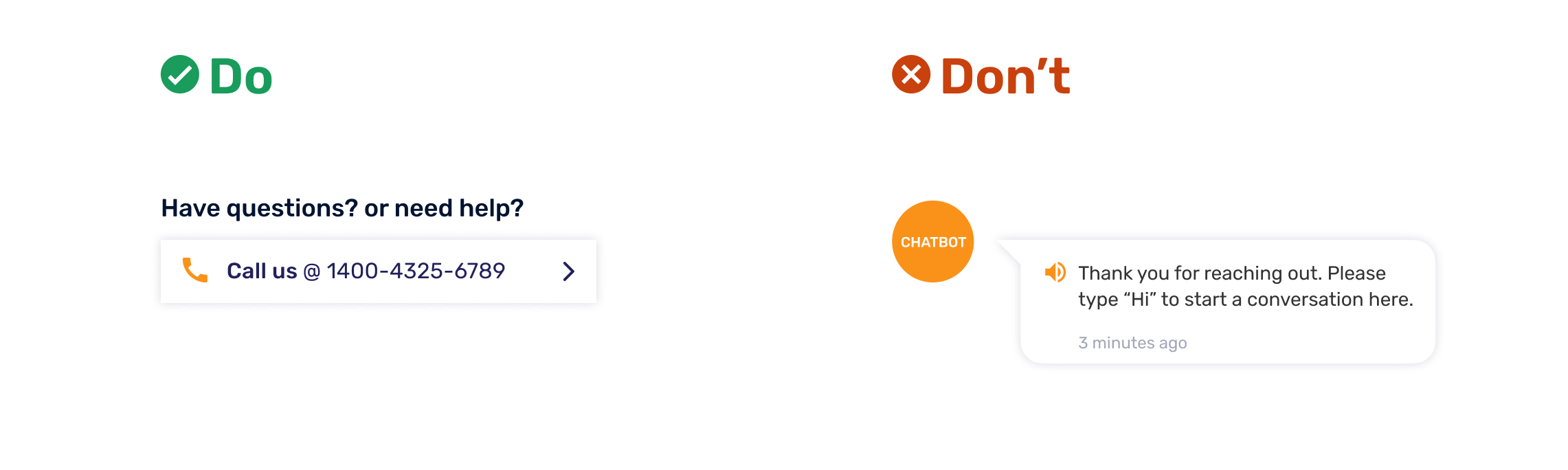

Chatbots are a big no for this cohort!

Forcing them to deep-dive into chatbot communication for help right in the beginning can lead to further intimidation. Instead, provide a vernacular help-line number they can reach out to so that they can have their queries answered and this sort of assistance can lead to continued usage and trust in digital products. Another way this could be explored is through voice UX for things such as payment confirmations as for them that is more reassuring than a screen pop-up with a green check mark. Moreover, some of them might not make these associations with colour unless the colours are embedded in a cultural context. Green doesn’t necessarily mean success to them. Try to introduce similar human elements as it helps new users build trust in the system.

#6 Storage

Ensure that your application doesn’t occupy too much space on their devices. Most of them own phones with minimum storage capacity and an app that gives rise to storage issues can lead them to uninstall it. Most new smartphone users are likely to have phones with nothing more than 32GB of storage. Considering the number of them who use phones purely for entertainment purposes, they’re most likely to delete a newly downloaded payment app, instead of the media elements such as photos or videos that they have captured. Therefore, design lighter apps that require minimal storage space to prevent it from being a hindrance.

#7 Localization and personalizing app experience

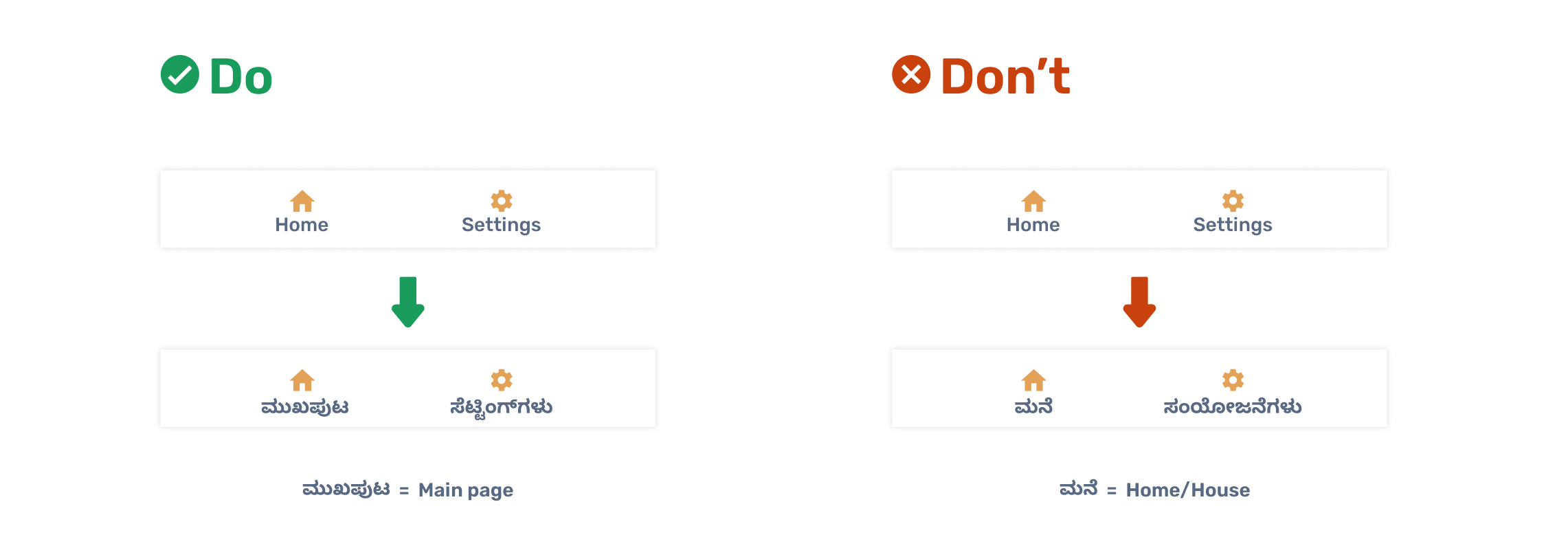

Try to provide an option for text in vernacular languages within the app. This can make things less intimidating for them by increasing comprehension. Apps limited to only English can make it seem complex to non-English speaking masses. Several people feel that English is a language that is for the educated and this becomes a barrier in itself and prevents them from trying out applications. Also, please avoid using the direct translation of words in local languages. For example, we as technologically savvy users are familiar with calling the main or first page of the app ‘Home’, but a direct translation of this in their local tongue will leave them beyond confused about this reference to a house.

#8 Test, test, and test again!

Translating insights from user research and field observations into usable elements in our product is no easy task. You seldom get it right on the first go. Therefore, conduct robust usability tests of your app with the target audience and observe their interaction with the product. This will give you a peek into what’s working and what’s not and will help you refine your design to make them more usable.

This will also help us design tailor-made features that are actually useful for them. For instance, in the context of vendors who have their customers pay adjacent store owners, can we look into streamlining this community aspect of payments for them? With the money being sent to the same person, how can we help them keep track of each other's separate pool of earnings?

#9 Digital literacy and community engagement

Beyond research, design, and development, the key to helping first-time smartphone users overcome the fear of new technologies is to educate them through digital literacy or community engagement initiatives so that it helps them become familiar with the product in general. Without this knowledge, most users are going to find technology intimidating as it is starkly different from their current ways of going about day-to-day transactions. Most of them are not aware of the value of the device they have in hand and the potential opportunities it can open up for them. Educating new users about the benefits is imperative and can go a long way in increasing adoption. Moreover, they are eager to learn and they can learn better with step-by-step instructions provided to them. People in this user group are unlikely to explore the app on their own as they fear they might do something wrong. Bring in the context of payments and the fear increases multifold.

Leverage the power of community. Conduct in-person or virtual sessions (in the case of smartphone owners) for a group of people within a community and educate them about new products that can potentially improve their lives. Once they see a few members in the vicinity reaping the benefits of these new developments, more users will be determined to try it out. Through campaigns, help them become aware of your app's use cases. Awareness about the practical value and impact of your product can go a long way in pushing users to try it out. Otherwise, low-value perception clubbed with usability challenges can lead to low motivation to continue using digital payments.

What role can user research play in designing user-centered financial products?

We are constantly influenced by the bias of our own experiences so it is impossible for us to blindly assume the experience of our users. To overcome this, talk to your target audience and you will be surprised by the unexpected angles that you discover. This approach will help you solve for their needs and can help increase user engagement with your products.

This study cemented my belief in the necessity to look beyond the design of screens or interfaces while designing products for first-time smartphone users. It is essential for us to step into their shoes to break down barriers to entry, build trust in the system, increase digital confidence and nudge users towards eventual adoption.

Quantitative data is incapable of capturing the nuances in people’s lives. It can tell you “how many” people took a particular action such as clicking on a certain button. But it cannot tell you how many clicked on it by mistake, what made them click on it, whether or not they were able to accomplish intended tasks, was it easy to discover the button in the first place, and other such details about their lived experience with the application. Only contextual immersion and observing users in their everyday settings can help us discover the actualities of their experiences.

Besides, following a more user-centered approach in which solutions are derived from people’s everyday experiences can help us nudge them towards adopting desirable habits.

Try to use a combination of the digital and non-digital aspects in order to achieve this.

Co-create with your users whenever possible.

Go on-field and try to involve the target users in the design process.

This creates a sense of ownership amongst them and are therefore more likely to adopt the product.

The way ahead

Rural smartphone and internet penetration increased 30% per annum over the last five years. This in conjunction with a significant reduction in data prices drove the rise in smartphone usage. Moreover, events such as demonetisation in 2016 and the Covid-19 pandemic pushed merchants to offer digital payment options and move to a less cash-intensive mode of operating.

This change in the status quo presents an opportunity to help new digital users make the transition towards using digital financial services and to help them understand the value of smartphones and the internet in adding value to their lives.

Limitations of the study

These insights are based on observations and research conducted among first-time smartphone users in a metro city and might not be a true representation of the practices prevalent throughout the country. In order to validate these findings further, an in-depth study with a larger sample population might be necessary.

All illustrations are designed by Prajna Nayak.

If you enjoyed reading this blog and would like to receive more such articles from D91 Labs, please subscribe to our Tales of Bharat blog here.

To know more about our work at D91 labs, visit our website!

UPI - Unified Payments Interface is an instant real-time payment system developed by National Payments Corporation of India.

Tooltip - The tooltip, also known as infotip or hint, is a common graphical user interface (GUI) element in which a text box displays information about a particular element when hovering over a screen element or component.

SVG - SVG stands for Scalable Vector Graphics. SVG is used to define vector-based graphics for the Web.