The fintech call for women-led businesses

Unpacking the role of fintech in driving financial inclusion for women-led businesses

From adeptly saving small amounts of money for personal expenses, intuitively managing the entire household income to running multi-million dollar businesses, women of Bharat have been forging their financial journeys and futures for centuries. Research shows that women-led Micro, Small, and Medium Enterprises or MSMEs have on average been found to generate higher profits and lower Non-Performing Assets i.e. failed loans when compared to their male counterparts. Women entrepreneurs have also been found to be relatively more trustworthy as customers of financial services.

This in itself would make a strong case for their inclusion within the financial ecosystem. After all, access to the financial market and the suite of products on offer allows companies and individuals to grow their wealth or capital and protects them from unforeseen events, which are key objectives of running a business.

However, the numbers on this paint an interesting picture of the gender skewed nature of financial markets. Of about 6 Crore MSMEs in India, about 21.5% are spear-headed by women. Most of these MSMEs fall within the micro sector, and are unregistered. When compared to the rest of the world as well, India has fared poorly, with lower than 5% of female entrepreneurship.

Figure: Total early-stage Entrepreneurial Activity (TEA) by gender (% women, % men).

Source: GEM Entrepreneurship Report 2021.

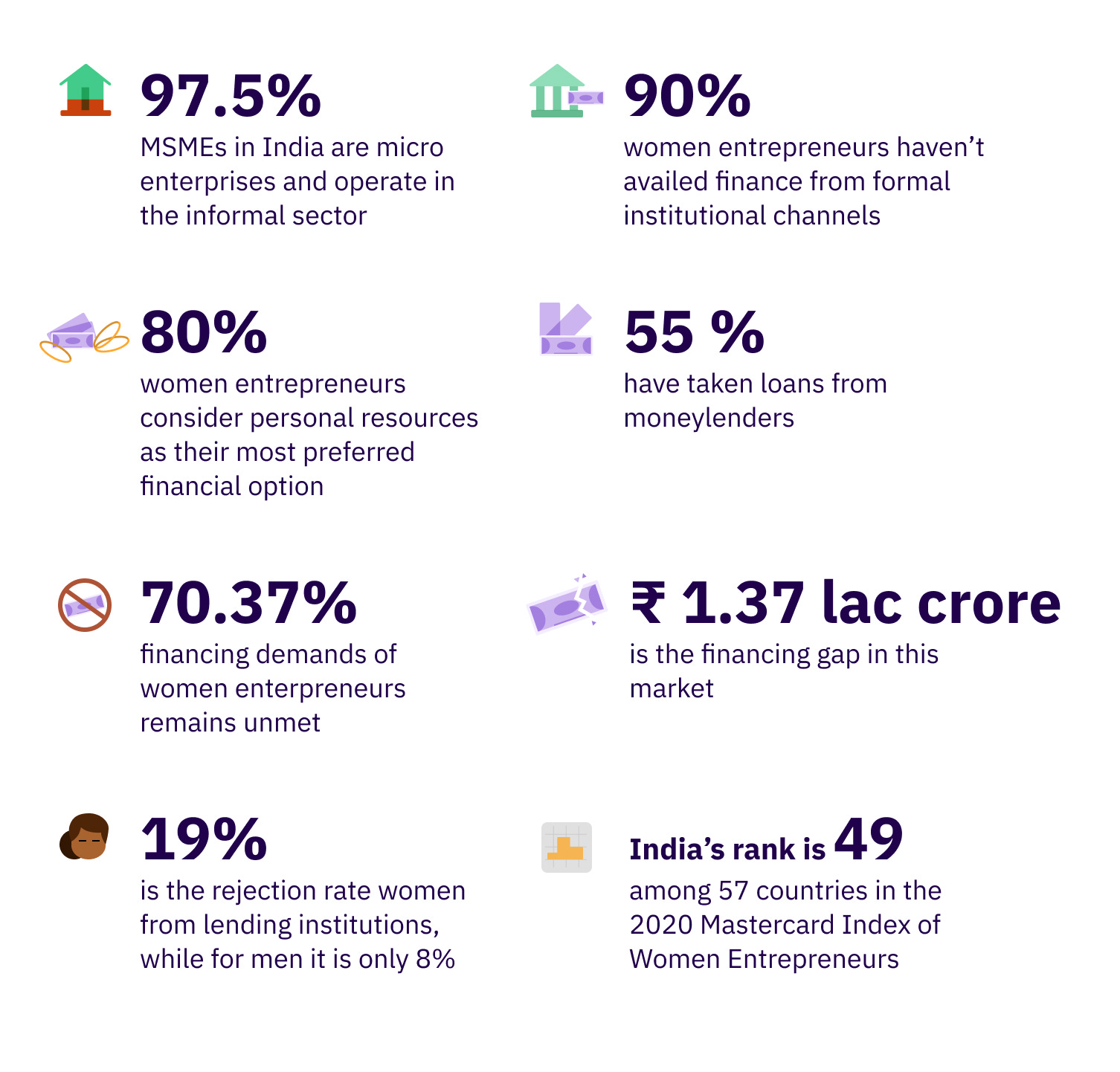

You may well ask, what about those women that are definitely entrepreneurially inclined? Is their ability to access the financial products and service i.e. their inclusion at least at par with their male counterparts? Well, let’s review some stats on that.

Sources: Financial Inclusion for Woman-Owned Micro, Small & Medium Enterprises (MSMEs) in India & The Mastercard Index of Women Entrepreneurs.

Well, then to what do we owe this disparity in their ability to access the market for financial services? In this article, we try to identify some of the reasons behind it and cultivate some insight into the manner in which we can resolve them.

So, let’s get to it, shall we?

Shining a light on the roadblocks for women-led businesses

MSMEs in India often face a wide variety of issues in their quest for optimising their financial journeys especially in their access to financial goods and services from formal sources i.e. banks and other financial institutions. These hurdles are compounded significantly if these businesses are women run or women-led. A brief snapshot of what these hurdles look like for women-led businesses especially in the MSME segment is below. While this cannot convey all of the concerns, they have been broadly bucketed for better understanding.

#1. Socio-cultural concerns

Let’s start with the basics and talk about the home front. Women often carry the burden of having to manage all household related care work. The survey undertaken by the National Statistical Office published in the year 2020 revealed that 81.2% of women in India are engaged in unpaid household work everyday. Across many sectors still, women are not typically encouraged to take up entrepreneurship or employment. There, continue to be many examples of women being harassed by family for their choice to work outside of the home, especially in fields which are predominantly considered male territory. An indicator of this is India’s female labour force participation, which is still amongst the lowest in the world.

In cases where women are employed, the sectors which have a significant participation of women in their workforce tend to be labour intensive and technologically limited. The seasonality/ irregular nature of labour requirements and the wage disparity all play a role in keeping women out of and away from the labour market. Finally, of the women that do run a business, about 78% of such businesses are based out of their homes, are sustenance based and are motivated by the need to have basic income and stability. Further, necessities surrounding marriage, movement on account of male-member transferring across geographies etc., and finally safety concerns determine the long term sustainability of these businesses.

#2. The long road from awareness to access

Away from the home front, efforts are being made towards better access and facilitation of the financial product pool through schemes and benefit programs by governmental bodies or financial institutions. The primary issue is lack of knowledge about the accurate value of the financial product/ services itself. Being unaware of the potential advantages of using these products for savings/ capital preservation leads to the preference of less optimal solutions like informal sources of credit, which tend to create debt traps and a vicious cycle for their businesses and lives due to the prohibitive costs. Preference for tried, tested and traditional methods such as savings at home or a reliance on no-frills financial product offerings is a direct consequence of lower levels of education, oppressive social norms, and the limited institutional impetus for educating women.

In part because of the above reasons and historical conditioning, formal financial institutions have been documented to have preconceived notions about women-led businesses being inherently more risky, unstable, and prone to shutting down. This gender disparity can often be found within the financial institutions, especially in the semi-urban, peri-urban and rural branches/ offices, where the proportion of women staff is also much lower. This leaves institutions with no incentive to bridge this knowledge gap and contributes even further to the awareness problem.

#3. Asset light, data poor and ill-equipped to handle risk

The third concern and probably one that plagues the MSME business segment generally also is the problem of data, collateral and risk management. The inability to provide adequate data and collateral quickly reduces the available options from formal sources. As noted before, most women-led businesses are in the micro segment and are unregistered, this makes the provision of both data and collateral a difficult one to comply with. Data usage for providing financial products/ services is to gauge identity and the ability to meet financial commitments that will form part of the access to services such as EMIs, insurance premium payments etc. Depending on the region, geography, socio-cultural background and literacy levels, availability of data (such as proof of identity, business registration, bank statements etc.) differs among women but in general continues to be limited. Further, collateral helps de-risk a lender. Collateral is unavailable to women entrepreneurs due to reasons ranging from unfavourable succession laws to the nature of businesses (asset-light) that women-led businesses are typically engaged in. Their possession of fixed or immovable assets is typically very low.

At the core of the inadequate access problem is the issue of risk management. Undertaking a financial commitment requires timely repayments/ premium payments and the ability to assess future risk that the business might face. The ability to manage this risk is a distinct requirement while utilising financial products and services. Women-led businesses often find it difficult to do so because of seasonal incomes, low literacy levels and inability to process long term business needs. Let’s take an example of insurance. Insurance helps businesses protect themselves from any future risks. The lack of awareness on the importance of insurance and the typically large outlays that have to be set aside for insurance premiums protecting them from unrealized events means insurance is often overlooked. This results in a vicious cycle of women-led businesses facing unforeseen events and having to borrow heavily from unorganized players, at a very high interest to cover losses.

Finally, add to this application processes that are cumbersome and complex often requiring physical verification of both information/ assets with terms such as male-signatory details etc.

Together, these concerns render financial products especially from formal sources fairly inaccessible to women running businesses.

Driving the future of inclusive financial markets for women-led businesses

In viewing the concerns identified above or elsewhere in your reading, a common thread is the systemic nature of most of the issues - some dating as far back as centuries and some more recent. Managing and improving upon these circumstances therefore is a concerted and enduring effort. With most such activities, it is also a long term endeavour. So you may be correct in wondering, what can we do right now? And the answer is, well, technology.

The growth of technology brings with itself the promise of inclusion. It enables us to overcome a lot of the stumbling blocks created by manual, low-data and biased financial processes that women entrepreneurs face regularly. The need of the hour therefore is a leapfrogging in the design, structuring and delivery of financial services. This is where the promise of technology and changing regulations can accelerate financial inclusions, especially for women-led businesses.

To that end, we have attempted to bring together certain guiding principles for creating and handling financial products for this segment of the population as they move along the financial inclusion spectrum. While these are in no way a solution to the systemic problems that women face each day, a better grasp of these, we hope will help bring better solutions to these challenges in the short and long term.

#1. Making women-led businesses data rich - the Aadhaar of it all

The two fundamental requirements for a data rich financial history are registration and a bank account. Attempts to simplify and streamline the MSME registration process are underway through various governmental initiatives, such as the MSME registration via the Udyam portal. However, the simplification of account openings for any number of financial services is a financial institution prerogative. Starting accounts should be streamlined using E-KYC, C-KYC and digital first and remote friendly setup by NBFCs and fintech players for women entrepreneurs who work from home or have mobility constraints but need financial services. By encouraging registration with government agencies, application of Aadhaar-based KYC and use of base products such as no-frills bank accounts as a first step, we can make women-led business “data rich” and open up the world of alternate products and offering to them.

#2. Alternative channels, data & products: Sachetization & product innovation

An extensive data footprint enables innovations in financial services. Here are some examples of that.

First, by utilizing digital public goods. Account aggregators, UPI & OCEN acting as new rails to the payments, data sharing & lending sectors, when leveraged by small-finance banks, fintech companies & NBFCs will enable these institutions to digitally & seamlessly serve payments and credit needs of women-led businesses.

Second, sachetization of products. Even during tumultuous times such as the COVID-19 pandemic, a study found that women entrepreneurs preferred debt-free monetary assistance and other low-risk financial products. What this suggests is a market for micro sized loans and insurance products. The creation of these new age instruments ranging from ‘Buy Now Pay Later’ to EMIs (card & cardless) & P2P lending, on the back of the gigantic digital public infrastructure already in place in India, has the potential to meet capital expansion and preservation requirements of women-led businesses.

#3. Augmenting and reimagining traditional financial services

Aided by digital channels, there has been a steady rise in women-focused business networks like Sheroes that provide tailor-made offerings as well as opportunities for women entrepreneurs. These are especially helpful because they have a mix of intangible support like networks, trust, guidance and more tangible finance-related support like short term loans.

For decades, women have depended on unorganized or semi-organized chits funds, SHGs and microfinance institutions. While they continue to function and serve them well, a digital makeover to allow for more efficiency, lower cost and hybrid setup is needed for these institutions too. Startups such as Chitmonks and MyPaisaa among others are leading the charge with this.

Finally, when alternate lending is not possible, traditional lending can be supplemented through models for shared collateral (amongst self-help groups (SHGs) & women entrepreneurial networks). An interesting case study of this is the DFCU Bank in Uganda where the bank created an investment club and savings scheme for women entrepreneurs.

#4. Making provision of financial services more inclusive

At the heart of all successful innovation is an understanding of the customer that it serves. The nature of issues faced by women-led businesses and their socio-cultural roots require some built-in filters that can help product development and marketing to better address the needs of women entrepreneurs across geographies. These filters act to wade out some of the inherent socio-cultural biases that the financial markets suffer from. We have listed some below, but this by no means is an exhaustive list.

Removing requirements for male-signatories when applying for financial products such as loans/ investment etc. must be removed.

Increased focus must be placed on multilingual and multimedia support for applications and other products. This becomes particularly important for those segments of the population that have lower literacy levels including women micro-entrepreneurs.

Efforts must be made to build trust by reassuring women entrepreneurs that a product is a regulated, trustworthy and accessible mode of finance. Institutional focus on having more women staff, having village level women representatives of the products as a bridge with local entrepreneurs can be considered.

Service and product developers catering to this segment need to ensure financial products and services offered are contextually explained at every step of the user lifecycle when users are new to finance. Armed with the knowledge of the entire product journey in advance, women entrepreneurs can make a more informed decision on whether to choose these products.

Simplistic as these filters may be, a focused effort in applying these to every solution/ product/ offering or service created can have a significant impact on moving the needle on addressing the socio-economic and cultural roadblocks to the inclusion of women-led businesses into the financial markets.

Conclusion

Despite the gravity of the inclusion problem, small steps taken collectively on the micro-front have potential to lead to some systemic changes for the future of women-led businesses. Testing the viability of each of the directives/ solutions above and its applicability to all or some women-led businesses will have to be undertaken. However, available solutions, fintech, legacy or otherwise have developed a one-size-fits-all approach, thereby leaving large groups of women-led businesses underserved. With a host of regulatory and technological tailwinds however, the system is ripe for an upgrade.

Technology allows for a paradigm shift in the delivery and structure of financial services that can accelerate financial inclusion for women-led businesses, improve their likelihood of success & lead to betterment of their lives. However, to do so also involves thoughtfully understanding the context, problems and points of friction that continue to affect women entrepreneurs. With empathetic product building and applied research, we can support them in becoming massive enablers for our economy.

It’s an exciting time to be a builder in the fintech ecosystem. What do you think can help improve access to finance for women-led businesses?

References:

Ministry of Micro, Small and Medium Enterprises, Annual Report, 2019–20.

International Finance Corporation, ‘Financial Inclusion for Women-Owned Micro, Small & Medium Enterprises (MSMEs) in India’, 2018.

Nilanjana Bargotra et al., EPW Engage, ‘How Did India’s Women Enterprises Fare during the COVID-19 Lockdown?’, May 2021.

Shreeja Singh, MoneyControl, ‘Insurance-averse MSME sector hit harder by Covid; experts call for higher coverage’, July 2021.

Krea University, ‘Women’s Entrepreneurship in India: Harnessing the Gender Divide’, February 2021.

International Finance Corporation, ‘Improving Access to Finance for Women-owned Businesses in India’, 2014.

Women’s World Banking, ‘Report: The Power of Jan Dhan: Making Finance Work for Women in India, August 2021.

Accion Insights, RBL Finserv, India MSME: Innovations to Increase Financial Access, December 2016.

Disclaimer

This article and its contents represent the views and opinions of the co-authors (Anushri and Atreya). They do not represent the views of their employer, institution or that of D91 Labs.

Anushri Uttarwar is a fifth year law student studying at the Jindal Global Law School and Atreya Arun works as an Associate Product Manager at MyGate.

All illustrations designed by Prajna Nayak.

If you enjoyed reading this blog and would like to receive more such articles from D91 Labs, please subscribe to our newsletter here.

| A guest post by

|

|

|