India ❤️s F.D and they need a digital makeover!

Why Indian startups don't distribute F.Ds?

As a kid, when my mom refused to buy me candies, I would run crying to my grandmother. She would console me and offer a 10 rupee note from the stash of money hidden in the rice jar. The entire act was nothing short of magic like a magician pulling out a rabbit from the hat. That carefully rubber-banded money was her secret savings which she could spend without owing an explanation to the family.

India is largely a savings economy. The idea of saving money for the future is ingrained in the culture. ‘Savings’, offer safety/ security for both planned and emergency expenses. Research shows that inadequate savings and the absence of appropriate insurance push households to borrow money from informal sources at higher interest rates during emergencies.

These informal savings come with their own set of shortcomings.

Inflation: Money loses its value over a period of time and the money though is under the bed does not automatically increase 🤭 (I know, it is sad)

Impulse Expenses: Access to liquidity is not always necessarily a good thing. It lures households to make impulse purchases that could potentially be avoided to save for future goals.

The 2016 demonetisation resulted in a hit on the savings of women in many households. These were the money that these women had saved secretly over years, typically from the monthly spending allowance received. The idea behind this was to save them from being spent on impulse purchases and use them for a large spend like kid's education or marriage. We overestimate what we can do in the short term and underestimate what we can achieve in long term.

Fixed Deposit - 👑 of formal savings!

Fixed Deposits (FD)/Recurring Deposits (RD) offerings from the banks is a magic product that overcomes the shortcomings of the informal cash savings. FD is the simplest savings product. They offer guaranteed returns with full capital preservation as opposed to other financial products like mutual funds and stocks. FDs come in all shapes and sizes. The investor could choose their periods of investment and modes of investments (SIP, Lumpsum). FD’s minimal friction to redeem pushes individuals to make an informed decision before withdrawing them before the maturity period.

In short, FD is the perfect product for the average risk-averse Indian.

Over the years, investing in FDs have become cultural wisdom that is passed on from one generation to the next

I started doing a post office RD after seeing my father having saved in such a manner. I heard it from my father but I did it myself. It helps me manage expenses during the Pujas and other occasions. I withdraw the amount during the Pujas. If there is anything left over, we do some shopping. - Protim, 28

I have 5 FDs. I have them in SBI. SBI gives me a very good rate of interest and my principal amount is 100% safe and secure with SBI. If we have some amount in my hand, say Rs 50000, Rs 1L, Rs 2L, Rs 5L, if I have a sufficient amount in my hand as cash, then I open an FD in a particular bank. - Manu, 37

When I opened the FD/post office account, I did not have anything in mind. I opened it for small investments whenever I get the chance. After 1-2 years, I will be able to submit a good amount in one of those accounts. Some seniors and parents also gave me advice - “When you get money, don’t waste it here and there by using other things. Invest small amounts for your future.” So I’m going on that ____, keeping a small amount like 50000 or a lakh. - Praneet, 37

In some cases, individuals choose their banking partner depending on the interest rates offered in their FDs

The main reason I opened my account here is that from Day 1 this bank is giving 7-7.5% interest. In the current scenario, all the banks are coming down to 5 - 5.5% interest for FDs & RDs but in IndusInd bank, it is still at 7%. So I have kept it for the purpose from the beginning itself - because I am getting a savings account interest that is much higher than other banks. Initially, it started with 7%, then it dropped down to 6% and now it is 5%...but still much better than other banks. This is beneficial for me for FDs and RDs. - Sushant, 37

Quotes from D91 Lab’s qualitative interviews. All the names of the participants are masked to honour their privacy.

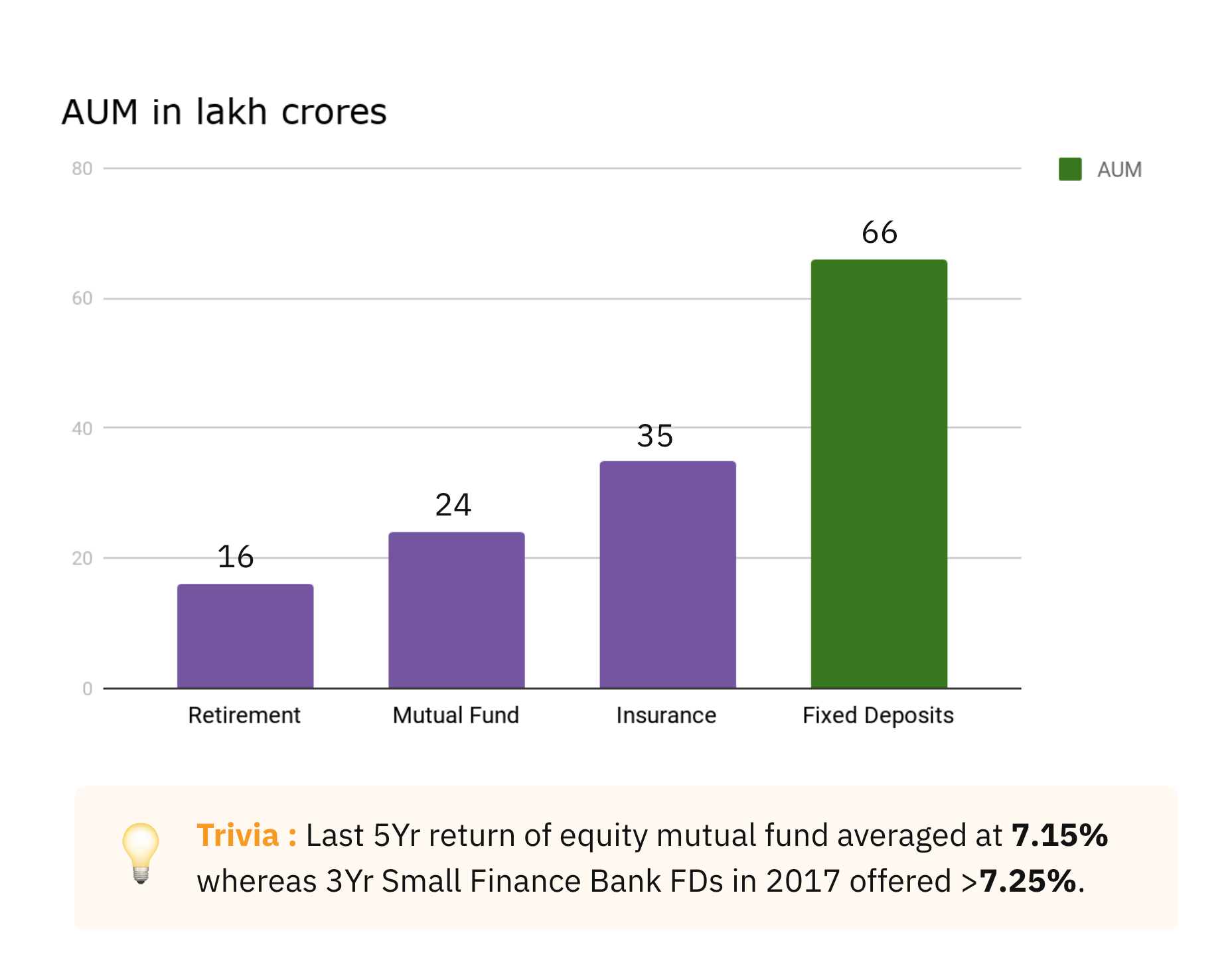

In fact, FDs have the highest amount invested among all the other savings and investment products in India

FD's are the most loved savings product of Indians and yet one cannot compare and invest in an FD across various banks through a single mobile app as one could do with mutual funds. Here is why?

Fixed Deposits need a modern makeover.

Startups like Zerodha, Paytm Money, Scripbox, and Groww have helped investment products to leapfrog to digital. Today even a noob investor has the ability to compare the performance of various mutual fund schemes from various Asset Management Companies (AMCs) and invest in one of their choices through a broker digitally. But one cannot invest in an FD in a similar fashion. FDs as an investment have largely been ignored by startups and there is a valid reason for it.

Challenges for a fintech to offer FDs as a product:

Bank account requirement: With an exception of a few small finance banks, most banks require the individual to open a savings bank account to start an F.D. Hence offering FD as a standalone product without a bank account becomes a challenge. To build a portfolio basket containing 5 FDs, you are forced to open 5 bank accounts. With each bank account open, the worry on maintaining a minimum balance & potential penalty increases. That’s bad and thankfully 2020 has nothing to do with it. It's an age-old problem.

Longer integration cycles: Unavailability of ready to consume standard APIs makes it challenging to individually collaborate with various banks and build a network of F.D APIs and distribute them.

Absence of standard business model: Unlike mutual funds, FDs as a product do not have a clear business model yet.

These challenges stop any new incumbent startup to distribute FD as a stand-alone digital product to the Indian investors. But the need for a digital FD is higher now more than ever.

Why the time for digital F.Ds is now more than ever?

Falling FD interest rates: Trend shows that the rate of interest has been steadily dropping over the years and people tend to move toward riskier investments like mutual funds in the lieu of higher interest rates. But the newer small finance banks have been offering higher interest rates as compared to a larger public and private sector banks. But the lack of awareness and the lack of trust and information becomes a challenge for the better return offerings FD products to pick up.

Pandemic and digital: The pandemic has forced most of the financial transactions to go digital and the surge in UPI transactions during the pandemic is a clear example of it. With that lens, the requirement for individuals to walk into a branch to open/renew an F.D seems like a pre covid thing to do.

Newer pockets of digital trust: The aggregators like Google Pay, Swiggy, Khatabook, and Meesho have already built trust among the users by demonstrating their value to the users in one way or the other. In short, they have become pockets of trust in the digital world. These entities become the perfect partner to combat the trust problem for the bank to distribute their FD product digitally.

By making FDs purely digital we will be able to unlock a whole new range of use cases starting from inculcating a savings behaviour in young adults to a newer use case likes consumer durable savings (similar to consumer durable loans except that one saves up to purchase a product)

Digital FDs will enable millions of household women to confidently save money for a better future digitally without the fear of being exposed. This is one of those 2020 wishes which we hope comes true by 2021!

This weeks newsletter is presented by Dharmesh Ba. Huge shoutout to my colleagues Krishna Hegde, Paul PJ, and Geetika Shukla who helped me put together this piece. If you are an aggregator who would love to offer F.D as a product, do drop us a note for and we would be happy to a jamming session. - Drop a note to paul@setu.co

About D91 Labs

D91 Labs is a user research lab, sponsored by Setu.co that specialises in financial inclusion research in India. D91 Labs aims to bridge the empathy gap between the fintech organisations and the last mile India through human-centred design methodologies. We conduct in-depth qualitative research to document the financial journeys of Indians across various socio-economic segments and publish them under open-source licenses for the fintech community to consume.

Paytm Bank should be here instead of Paytm Money - They have FD - super liquid

Great piece with a simplistic explanation. Since the necessity of multiple bank accounts is an impediment to FD investments. Can one account and option to choose fin products from different banks with that account can be a solution? And if it can be, what are the problems we are facing to reach the level of a unified account system?