Credit where credit is due - Enabling MSME businesses through the AA framework

How the AA framework opens up new avenues & greater efficiency for MSME lending.

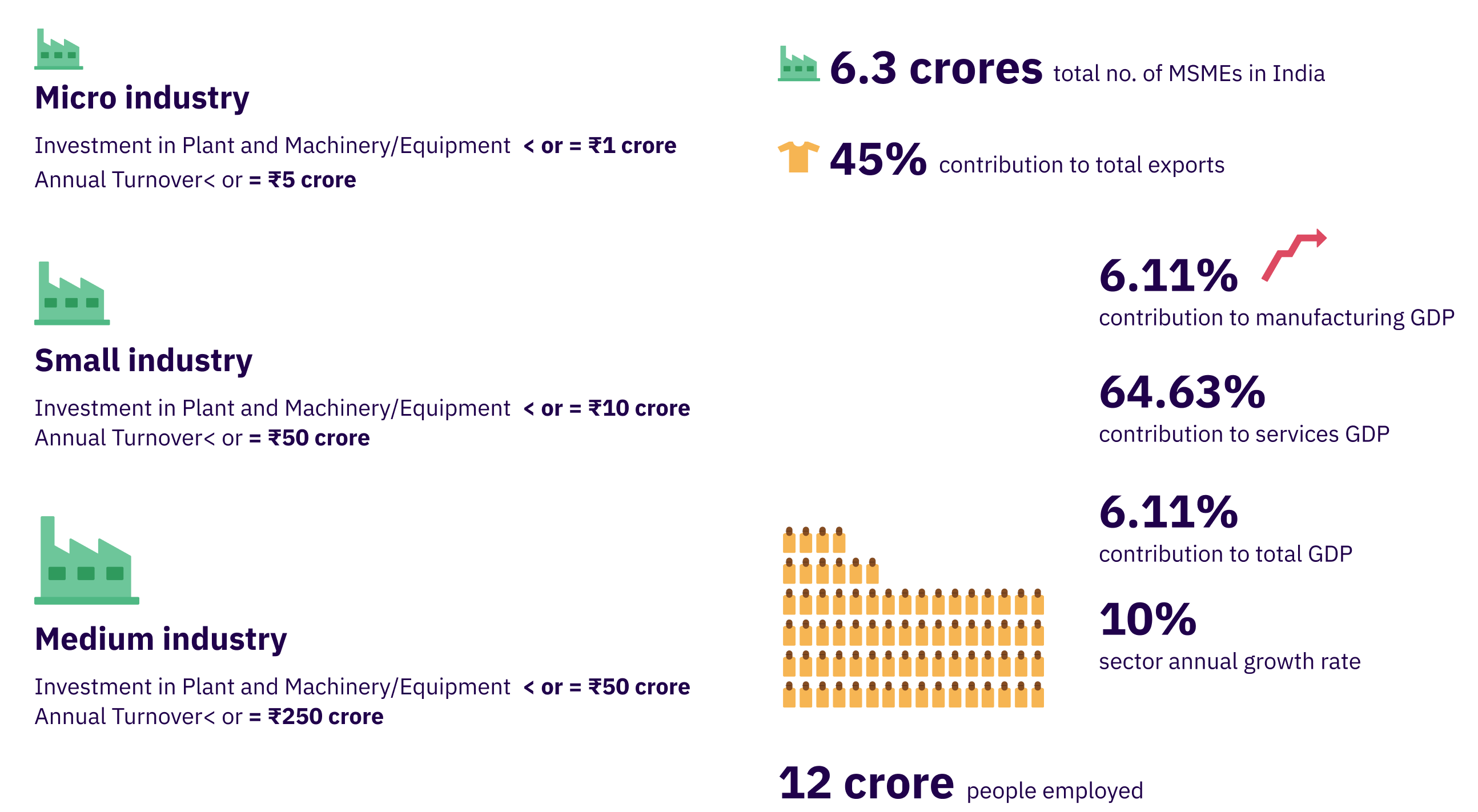

MSMEs a.k.a. micro, small and medium enterprises are undeniably the lifeblood of the Indian economy. What’s more? About 20% of MSMEs are rural-based, which means a significant section of deployment of MSME workforce is rural. This makes the MSME sector a beacon of sustainable and inclusive development.

However, despite their significant relevance and contribution to the Indian economy, MSMEs continually face a surge of systemic and sector-specific constraints. These were categorically highlighted in the PM Task Force Report of 2010 and can be generally referenced in three broad buckets.

First, regulatory and governance concerns such as inadequate infrastructure, complicated compliance processes for registration of enterprises, and taxation.

Second, market access concerns such as lack of skilled manpower, limited approach to global markets, and low penetration of technology.

Third, access to credit concerns such as high cost, collateral requirements, lack of timely and adequate funding for both debt and equity.

In the decade that has gone by since the Task Force Report was first published, steps have been taken to address the combined issues of market access and regulatory governance. While these have led to significant progress and simplification of the business life cycle, the credit gap continues to remain a critical roadblock.

Sources: Ministry of MSME - What’s MSME?, CII - Micro, Medium and Small Scale Industry and IBEF - Sector Update, May 2021

The fact that MSMEs represent a diverse cohort of enterprises that find themselves functioning across a wide spectrum of financial and digital inclusion remains as true today as it was a decade ago.

Interestingly, with the penetration of fintech products across sectors, the low access to technology for cohorts in this sector poses a serious challenge to improving credit access. With pioneering fintech products clamouring to service the MSME sector, the account aggregator (AA) technology has the potential to unlock the maximum benefits of this keen fintech focus on MSMEs.

So, let’s dive in.

The big MSME credit gap

To start off, MSMEs like all businesses require credit to accomplish two primary goals - working capital funding and business expansion or fixed capital investments. Typically, working capital funding is short-term and more flexible while business expansion and fixed capital investments are medium to long-term requirements. Traditionally, formal sources of credit for all businesses have been banks and NBFCs that rely on asset-based models and past performance data for de-risking and collateralization. Further, their brick and mortar setup increases their cost of lending which gets passed on to the consumers, and finally, these formal financial institutions require a wide variety of data sets often in physical form, hand-delivered and self-attested.

We have looked into each of these lending pre-requisites in some detail below from the MSME lens to determine the source of the credit gap.

#1. Formal financial markets hinge on de-risking by collateralisation.

Financial institutions that lend money to businesses often need to deleverage themselves through asset collateralization. This, to ensure that if the repayments are derailed, they have the ability to sell these collateralized assets and obtain the disbursed funds. For MSME businesses which are often asset-light, another option is cash-flow-based lending. In this form of financing, the future projections of a business are used as a yardstick for determining its ability to repay. Even though cash flow-based financing is not a new concept, financial institutions under most circumstances are unable to verify the projections provided by the MSME and therefore unable to justify their credit underwriting decisions. As a result, MSMEs tend to remain underfunded by formal financial institutions, especially for their long-term capital expansion requirements.

#2. Trust is a two-way street - data begets data

Another important contributing factor to the credit gap is the lack of solid data on the business, practices, and potential of an MSME. Under regular lending circumstances, a financial institution will determine whether to underwrite a loan or not by requesting some or all of the following information:

Identification proof i.e. KYC documents relating to the proprietor and the business.

Proof of financial health and future projections i.e. bank records, P&L statements, cash flow, revenue and balance sheets etc.

Proof of past financial performance i.e. bank statements, payment records, cheque bouncing and EMI payment history etc. along with the relevant credit score.

Each of these factors gives the lending institution an indication of whether the MSME and the proprietor have the willingness to repay, which is the second principle of creditworthiness. However, data is not always forthcoming. Even as late as 2019, the private credit bureau coverage (and consequently the availability of credit scores on businesses) in India was as low as 63%. From an MSME perspective, there is fear that the data might be misused and the formal structures and perceived distance between the financial organization and the proprietor or MSME creates a sense of distrust that is hard to bridge.

This lack of verifiable data and credit history leads to denial of access to credit which does not allow the MSME to create a stronger pool of data and credit history and that becomes a vicious circle that feeds into the credit gap.

#3. Lending is a costly endeavour

Most formal financial institutions currently function as a combination of brick and mortar offices/ branches and online or app-based banking. Despite their burgeoning online presence, in most sectors, especially MSME, the style of conducting business is old-school. While servicing specific sectors and rural and peri-urban areas, traditional lenders focus much of their business & outlay on having physical operations for onboarding, collections, and interfacing directly with borrowers. This is in part due to the requirement of customer assistance while conducting businesses in these sectors/ regions. As a result, the cost of acquiring customers while maintaining physical branches is very high. The operational cost is then passed on from the lender to the customers that they serve. In the case of MSMEs, this operational cost becomes prohibitively high on account of the low-ticket size of this customer segment and makes for a discouraging statistic for such institutions to work off. Finally, given the lack of active reliance on digital solutions, and often in spite of that, there is a continued reliance on physical collection and delivery of data such as the documents mentioned earlier. This adds a time cost to the process which also impacts the viability of servicing the MSME sector efficiently.

What remains therefore is a choice to either leave this customer segment un-serviced or charge very high rates to justify the business. A lose-lose proposition for the MSMEs leaving them little choice but to borrow from informal sources with exorbitant interest rates, leading to over-indebtedness.

That begs the question of whether there is a better solution.

Digital solutions for MSME lending.

With the advent of digital lending newer players seem to be filling in the gaps in credit supply. Fintechs and some NBFCs, with their improved technology and distribution channels possess a few distinct advantages:

#1. Cash flow/ revenue-based financing

Rather than a standard asset-based loan format, typical of banks and NBFCs, digital lending solutions can leverage improved technology and data access allowing them to use models like cash flow based financing or revenue-based financing (mode of financing where the repayments are made as a percentage of future revenue of a business) to their full potential.

#2. Improved distribution channels and lower lending costs

The channel in which these loans are disbursed ensures it's often easier for them to reach customers. MSMEs can simply apply for these loans from their place of business. This drops the cost of servicing the loan. Digital lenders spend only notably lower on customer acquisition as compared to their traditional counterparts.

#3. Better data handling

Digital lenders are able to handle data more efficiently and cost-effectively. MSMEs just have to provide the documents online, and the actual underwriting that these players tend to do is better given their data processing competency and readiness to utilise alternative data sources. However, it is also important to recognise that this data handling is only as good as the available data on the MSME. It is in this context that various governmental interventions and schemes that are boosting the use of basic technological tools such as no-frills bank accounts for receiving direct scheme benefits or online registration of all new MSMEs etc. are blazing a trail of online data presence for these MSMEs. This has a trickle-down benefit of allowing better digital products to be created for them including those for bridging the credit gap.

Applying the AA framework towards optimising the credit needs of MSMEs

As is evident, the benefits of the digital platforms servicing MSME debt requirements are actively linked to their ability to access, process and utilize data about the business, its financial health, its performance, and most importantly, its future potential. Despite their obvious advantages, even digital lenders face challenges due to non-standardized and incompatible data formats that don’t allow them to use their technology to its full potential.

This is where the AA framework comes in. As the latest addition to India Stack, AAs possess a consent-based and timely data sharing capability. This digital public good allows for increased efficiency and accessibility, for a wide category of data-sets and as such has much to contribute towards narrowing the credit gap in the MSME sector.

Let’s take a hypothetical example and see how.

Suneet is a wholesale trader from Maharashtra with a relatively perennial business with moderate-to-low volatility and festive seasons showing higher sales or revenues than other months. In 2022, Suneet intends to expand his business by availing a credit line of up to Rs. 50 lakhs. However, because he works in a rented warehouse, he is unable to provide physical assets as collateral for this loan.

While he has a choice to approach any bank or financial institution, Suneet has chosen New Finance Ltd. a fintech lender, who uses a combination of mainstream and alternative data to engage in cash flow/revenue-based financing. New Finance Ltd. has recently become a financial information user that relies on AAs, to easily access consented data directly from Suneet’s accounts with financial information providers (i.e. banks where he holds his accounts, investments made in FDs, and RDs among others.)

We have put together a quick tour of what the loan application process for Suneet’s business would look like.

Choosing the required data c/o AAs.

As seen from the snapshot of Suneet’s company and his finances, the business has fairly healthy metrics and finances. The data sharing control always remains with Suneet and will involve the New Finance Ltd. & Suneet coming to an agreement on - the kind of information, the frequency of provision and the duration for which it will be provided. Based on the above premise, a lender like New Finance Ltd. would typically request for the following data via an AA:

With this, lenders like New Finance Ltd. can successfully profile the risk levels of lending to Suneet’s business. Based on this, they can choose an interest rate, terms and conditions for the loan and be assured that they have accurate data across the repayment period.

Making the underwriting decision.

On the basis of the available information and data, New Finance Ltd. decides to disburse Rs. 50 lakhs to Suneet’s MSME business through a revenue-based financing model. If Suneet’s enterprise makes average revenue of Rs. 6 crore across this financial year & the next, the loan can be repaid in full even with revenues that vary from month to month as long as the agreed-upon share of revenue is paid. This share of the revenue can either be fixed or variable depending on the seasonality or collections that Suneet’s projections show.

So what makes this combination of AA & alternative forms of lending far more viable for someone like Suneet?

With AAs coming in to the picture, however, the digitized & consented data sharing combined with cash flow/ revenue-based financing solve the key problems mentioned above:

A host of alternate data along with traditional sources (ranging from one’s own bank accounts, to GSTN data via their GSPs, to the deposits in the name of the business, utility payments, etc) allows for far lower operational overheads and better underwriting for the lender.

Information which was otherwise available to the lenders on-demand or on the principle of trust from the borrower such as regular cash flow statements/ bank statements etc. is available with consent directly from the source i.e. the financial information provider in a friction-free & real-time manner leaving limited room for trust mismatches allowing lenders more confidence to lend out to a more diverse set of businesses.

Continuous data access means they can set up early warning systems should the company’s returns data or bank statement fall below a given threshold balance or if they see irregularities. This can have a positive impact on reducing the risk of these loans turning into non-performing assets for the lenders in a customer segment where bad loans are fairly common.

From Suneet’s perspective, the prime benefits of this arrangement are:

The collation and provision of information and data on a regular basis is streamlined leading to an efficient and almost automatic system of data upload and processing. The manner of provision and handling of data being transparent and consent-driven reduces the mistrust with the financial institutions allowing Suneet to focus on the core business. It also reduces the time taken for processing the loan application allowing some much needed flexibility in decision-making.

Due to the projections and cash flow based lending, the loan product can be customized and tailored to the specific requirements of Suneet’s business taking into account the seasonality if any, and the repayment cycles can be arranged on the same flexibility principle without diluting in any manner the credit underwriting on behalf of the lender.

In summation

The actual math, terms & implementation of any loan disbursement are likely to be contingent on the nature of the business, the specific projections, and the lender’s expected return on investment. But, the idea that better data access through AAs can lead to increased loan access for MSMEs that are otherwise strapped for options is a starting point for a series of innovative solutions for MSMEs & lucrative business opportunities for lenders. With the advent of digital lending, traditional lenders are also embracing such technologies to smoothen the lending process, pushing the envelope on access and usage of better, simpler and more efficient financial services.

As more and more users embrace AAs as the future of data sharing, there are boundless use-cases to be discovered and perfected in the world of finance and beyond. As with any smart digital public good, AAs can possibly be ‘credited’ for the more focused digital and therefore financial inclusion of the MSME sector in India.

References:

Report of Prime Minister’s Task Force on Micro, Small and Medium Enterprises, GOI, 30 January 2010, Pg. (ii).

MSME Industry in India, IBEF - May 2021.

Notification - Credit flow to Micro, Small and Medium Enterprises Sector, RBI, July 2020

IFC Report - Financing India’s MSMEs, November 2018.

World Bank, Doing Business Project - Private Credit Bureau Coverage, India.

Micro, Medium and Small Scale Industry, Sectors, CII.

Ministry of Micro, Small and Medium Enterprises, What’s MSME?

Sahamati, Empowering Alternate Data Collection for Digital Lending with Account Aggregator Framework – Introduction, June 2021.

Global Alliance for Mass Entrepreneurship - Unlocking Credit for India's Job Creators April 2021.

Bridging the data gap one consensual data transfer at a time, D91 Labs, August 2021.

Unicornomy, Revenue Based Financing Business Model, Economics & Investment Rationale, August 2021.

Disclaimer

This article and its contents are completely the views and opinions of the co-authors (Atreya and Neeti). They do not represent the views of their employers .

Atreya Arun is a product manager at Setu and used to work as an Associate Product Manager at MyGate (at the time of writing this blog) and Neeti Bhatt was a Senior Research Fellow at D91 Labs.

All illustrations designed by Prajna Nayak.

If you enjoyed reading this blog and would like to receive more such articles from D91 Labs, please subscribe to our newsletter here.

|

|